Money management is one of the trickier aspects of freelancing.

Here’s the reality of this path we’ve chosen:

- Our revenue fluctuates – sometimes wildly, often unpredictably.

- Since we usually don’t know how much money we’ll make weeks or months from now, planning is difficult.

So I cringe when I see reductive advice in this area – for example, “Just set up regular payments to yourself!”

How can I set up regular payments if I can’t reliably forecast my income? And if I get a big check from a client, why would I parcel it out in increments? I’d rather get it into my greedy little paws immediately, so I can put it to better use.

Over the years, I’ve devised a simple system of managing and moving my freelance money. Today I’ll share it with you.

(Very Important Disclaimers: I’m not a financial professional, and parts of this may apply to the U.S. audience only.)

Managing Your Freelance Money: What You’ll Need

The system requires four accounts for your money:

Business Checking

The IRS, shall we say, frowns upon commingling. So I recommend keeping an account exclusively for business income and expenses. This also helps to maintain an important psychological wall between “business” and “personal.”

I also recommend incorporating, for the layer of protection it provides. (My business is an LLC.) If you’re incorporated, a vindictive client can’t come after your personal assets, and that’s reason enough for me. If someone wants to sue me for all my business is worth, they’ll be disappointed by how small that number is, as we’ll see shortly.

Personal Checking

You probably need one of these just to get through life. Here’s the problem: The interest rates suck. So I keep only enough money here to cover about the next 30 days of personal expenses.

High-interest Savings

This is where I keep about six months of living expenses, for two primary reasons: The psychological benefit of knowing it’s there, and the practical benefit of being able to refuse bad gigs or fire bad clients. (This is sometimes called your “freedom fund” or “F.U. fund.”)

This is also where I set aside money to cover my quarterly taxes and any upcoming retirement contributions.

There are plenty of high-interest savings options online. Lately, as the Fed has increased interest rates, these rates have increased too. Currently, some have annual percentage yields (APY) of 4% or more.

Brokerage

I recommend exploring the options to lighten your tax load by contributing to a SEP-IRA, a personal 401(k), or a similar vehicle. (Again, I’m not a financial advisor, but the pre-tax benefits can be significant.) You may also wish to invest some money over and above your freedom fund.

Finally, you’ll need some method by which to track your account balances. I use a simple spreadsheet to project the next six months, and I assume that expenses will be about the same. I project income conservatively; nothing is plugged in until the contract is signed, and even then, I assume payment will be a little late.

Managing Your Freelance Money: How It Flows

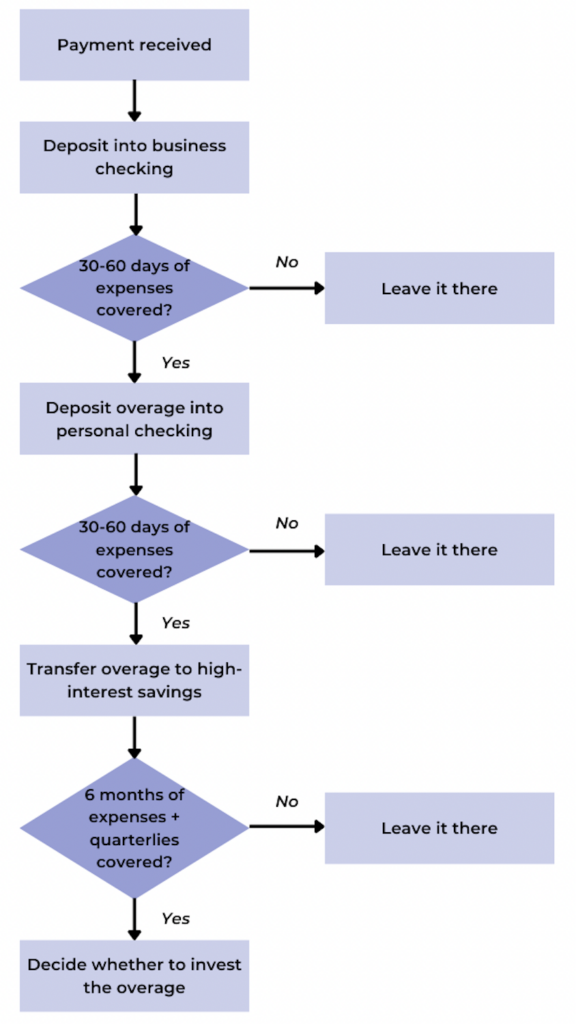

Here’s how it works in practice. Just ask three questions and take the implicated actions.

It starts when you receive payment from a client. Hooray! This money is deposited into your business checking account. Bottles of wine are opened, singing and dancing ensue.

Question 1:

Do you have enough to cover your next 30-60 days of business expenses (while also factoring any other guaranteed income)?

If no, leave the money in your business checking.

If yes, determine how much you can pay yourself, cut that check as soon as possible, and deposit it into your personal checking account.

Question 2:

Do you have enough to cover your personal expenses for the next 30-60 days?

If no, leave the money in your personal checking.

If yes, transfer the overage into your high-interest savings account, even if just for a few weeks. Better to have it making a little money there than sitting in your checking account earning nothing. As needed, you can always transfer some back into your personal checking.

Question 3:

Do you have enough in your high-interest savings to cover six months of living expenses, upcoming quarterly taxes, and retirement contributions?

If no, leave the money in your high-interest savings.

If yes, consider whether you want to invest the overage in the stock market. Again, I’m not a financial professional, but in general, the market will give you better returns than even your high-interest savings account. Of course, the associated risks are also greater.

My first rule is “don’t invest in what you don’t understand.” So I don’t dabble in stock-picking, and I have zero interest in crypto. I invest in index funds, which allow me to “buy the market” on a small scale. Simple.

And that’s it! You now have three simple questions you can ask yourself every time you get paid. And while you might tweak the specifics – you may, for instance, be more comfortable with more than 30 days of expenses on hand – the overall flow should work for you in most cases.

Here’s how it looks in practice:

Try it out yourself. Let me know how it goes, and let me know if you have questions.

Your time is valuable, and I hope I’ve rewarded it. If so, your shares are greatly appreciated, as I try to spread the gospel to as many freelancers as possible.

I have a limited number of slots available for 1-1 coaching. I’m not some guy who’s been freelancing for a minute – I’ve been doing it since 1997, with brands you’ve actually heard of. Click here to find out more about how my customized coaching can help you level up.

Copyright 2023 – Matthew Fenton. All Rights Reserved. You may reprint this article with the original, unedited text intact, including the footer section.